Dear Readers,

In last week’s blog (https://soumendaslive.com/2020/05/31/post-covid-19-prediction-for-crisis-prone-industries-part-i/) I had build an analytical framework to select three industries which have historically been vulnerable to a global crisis and studied their response to the past crisis to predict their possible response to the current Pandemic. I had mainly selected them based on a three point criteria system of :

- Systemically Important

- Vulnerability to crisis

- Long time frame to recovery

In today’s blog I would add three more industries which are particularly fragile and react adversely and fast to any crisis.

1. Retail Industry:

In every big crisis the Retail Industry gets impacted in the following way:

a. Logistics disruptions: The roadblocks on free movement of goods and materials disrupts the entire chain. It creates uncertainty in the minds of the retailers and thus they hesitate to take purchase orders from customers.

b. Supplier production disruptions: If the rate of production of raw material gets affected by a disruption, it cascades into delay in arrival of finished goods at the stores. This leads to low sales for the retailers.

c. Demand disruptions: A major crisis often creates disruption in consumer demands with spikes for certain items and no takers for others. This affects planning at the firm level.

Retail Industry Post SARS in China:

The current Pandemic has some similarities with the SARS epidemic of 2003 which hit China and parts of South East Asia. The epidemic had more than 8000 cases in China itself with more than 800 fatalities. Factories, Shops and Schools were ordered to close thus turning busy cities into lonely streets. The retail sector was one of the worst hit during the SARS epidemic. According to the National Bureau of Statistics of China retail sales plummeted to 4.3%, one of the slowest pace in years.

Birth of e-Commerce giants in China :

In 2003 e-Commerce was beginning to emerge in China with gradual increase in number of people with access to the internet. At that time e-Commerce was relatively primitive. Employees had to manually pen down orders and send text messages to customers when orders had been shipped. Employees personally delivered orders to customers who were close to the office.

There were two Chinese firms that got the maximum benefit of the crisis. The first one was Alibaba which was primarily a B2B platform, connecting U.S. buyers with Chinese suppliers. The second firm was JD.com which was a chain of small electronics shops.

Alibaba launched in 1999 had managed to have only 500 employees by 2002. It was planning to launch platform to compete with eBay but news of an employee being infected with the virus forced Alibaba to put all its 500 employees under quarantine. Workers took their desktop home to ensure Alibaba’s business-to-business e-commerce platform remained up and running.

As many countries around the world issued travel warnings for businessmen traveling to China, many turned to Alibaba’s online business to source Chinese goods. Starting in March 2003, Alibaba’s B2B e-commerce business added 4,000 new members and 9,000 listings each day, a 3-5x increase over the pre-SARS rate. Chinese suppliers, faced with few options offline, also invested more in online marketing on Alibaba’s platform. Alibaba’s business grew 50% that year and was seeing daily revenues of 10 million RMB. Over half of the 1.4 million suppliers on the B2B platform saw strong sales growth.

During this period Alibaba decided to complete its project of launching a platform to compete directly with eBay which was the undisputed leader at that point in time. Alibaba launched Taobao site on time, on May 10, 2003 in the middle of the epidemic. As people across the country were staying at home out of fear of contracting SARS, they turned to Alibaba to order items. The rest as they say is history, Alibaba went on to become an e-commerce giant .

JD.com on the other hand resorted to selling electronics on internet forums and QQ chat groups to keep the business afloat during the SARS crisis. It later devoted the bulk of the resources to the online business, growing it to become China’s largest online retailer of electronic products. JD.com which launched its portal in 2004 went on to become huge.

The two firms capture more than 72% of the e-Commerce market in China with combined sales exceeding $100 Billions.

Source : eMarketer

Post Pandemic Prediction :

Short Term : SARS gave birth to e-Commerce giants, COVID-19 would continue to boost the trend towards adoption of online as preferred mode of shopping in coming weeks. Brick and Mortar retailers would do themselves good if they adopt online method of delivery.

Medium and Long Term: In medium and long term as the Pandemic come under control, shoppers would return to offline shopping with possibly a different set of behavioral bias. The Retail firms will adapt to this either through organic restructuring of their business or inorganic mergers and acquisitions.

2. Housing and Real Estate Industry:

Housing and Real Estate gets an immediate knock on punch with every global crisis. Customers fearing an imminent slowdown in the economy postpone their buying bringing a slowdown in demand which cascades into multiple issues from laying off workers to filing of bankrupcy provisions.

U.S Housing Market after 2008 Financial Crisis:

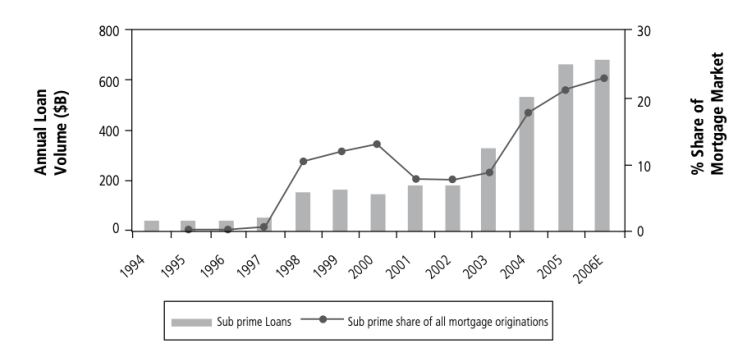

In the last decade of 20th century and early 21st century U.S. domestic and international policies increased its Government spending and deficit. This deficit was funded by additional treasury securities which further widened the deficit. It led to abundance of dollars in the market. U.S. financial institutions flushed with cheap dollars looked for high yield in the low credit sub prime (low income home buyer) mortgage market.

Source: Inside Mortgage Finance as published by the Center for Responsible Lending

Low interest rate had tempted low income American people to start buying house on loans. These loans were securitized (sold to investors) by bankers. The whole process was complex, interconnected, and vast—and it was all based on the hope of increasing home prices. As economic environment changed and rates increased sub prime borrowers started to default on their loans. This caused massive losses to banks and other financial institutions.

The crisis put an abrupt end to the goal of homeownership in U.S. The rate of foreclosures (foreclosure refers to loss of title of home by a defaulting mortgage borrower) increased dramatically leading unto 2007-08 crisis. The housing bubble burst and prices heading south.

Loose Monetary Policy and Quantitative Easing:

The Federal Reserve launched its Quantitative buying program in 2008 and started buying financial assets. The loose monetary policy of the Federal Reserve post the 2008 crisis restarted the low credit cycle leading to inflating housing prices again.

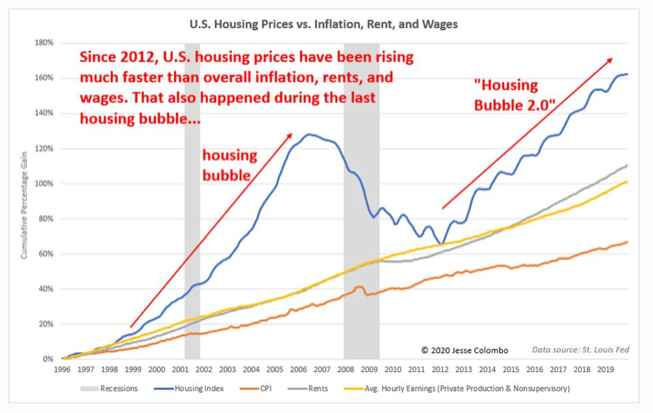

According to data published by the Case-Shiller U.S. National Home Price Index, housing prices have surged by 59% since their bottom in 2012:

Source : Case-Shiller U.S. National Home Price Index

As the chart below shows, U.S. housing prices have been rising much faster than overall inflation, rents, and wages, which is exactly what happened during the last housing bubble.

Source : Case-Shiller U.S. National Home Price Index

March traditionally has been the best performing month for the mortgage market in U.S. but this year the Pandemic changed it. Pending home sales fell 21% in March, and the National Association of Realtors projected sales to decline 14% for the year. By late April, mortgage applications had plunged 31% compared with the same period a year earlier. And all of this would have been much worse had Congress and the Federal Reserve not stepped in.

Post Pandemic Prediction:

Short Term:

In the near term the response would primarily depend on three factors

- How far will lenders go to minimize the number of forced sales? Forced sales quickly translate into falling house prices as we saw in 2008;

- How badly will borrowers’ incomes be hit and for how long?

- How much and for how long will real incomes fall?

Like nearly all artificial market rally, U.S. Housing Bubble has inflated faster than the underlying fundamentals. The current pandemic could be a catalyst to crush housing prices again.

Medium and Long Term: If the virus containment takes longer than anticipated, it could have bigger consequences for the housing market. Uncertainty could force household and businesses to hold on to cash and postpone buying property.

In the medium to long term it is expected that the virus will be contained and the economy would stabilize, which would make the home prices rise again.

3. Micro, Small and Medium Manufacturing Industries:

The final section of today’s blog is dedicated to the MSME sector which in a way is the backbone of all supply chain and global trade. The financial crisis in 2008 hit small businesses hard—in fact, harder than large firms. Many small businesses went under or were forced to lay off employees, slash spending, halt expansion plans, and find new ways to survive until the financial crisis subsided. In developing economies such as India MSMEs make a significant contribution to local employment and to overall gross domestic product (GDP).

MSME sector in India after 2008 Financial Crisis:

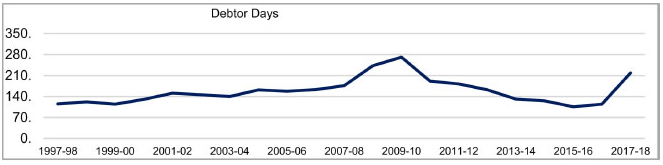

The MSME sector got a booster shot post 1991 liberalization when the Government reduced lot of hurdles and allowed outside capital to flow into India. The number of MSME’s grew from 6.7M in 1991 to 11.5M in 2003. Prior to the financial crisis of 2008, the sector contributed 7.2% of the GDP. But as the crisis became prolonged it started to hurt the Indian economy as deleveraging and risk aversion took center stage. As a result MSME started to feel the crunch of liquidity and demand. As global exports decreased and payments were delayed, Banks fearing risk of no return, reduced its lending to the sector. The below graph shows a jump in number of days during the financial crisis in receiving payments.

Source: Reserve Bank of India MSME Report

India’s central Government and the central bank reacted to the MSME liquidity crunch by providing liquidity to the sector. The Government through its fiscal policy announced credit facility for the sector. The Reserve Bank of India (Central Bank) through monetary policy made access to liquidity easier.

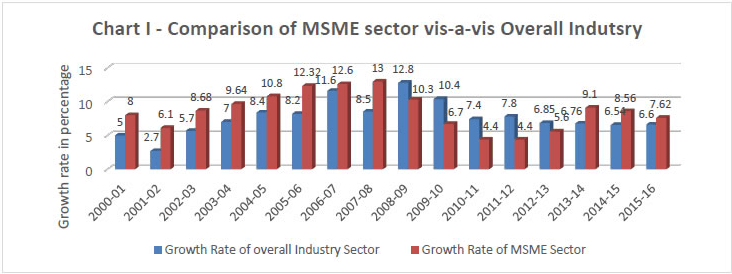

The below chart clearly shows MSME took several years to recover from the crisis.

Source: Reserve Bank of India MSME Report

MSME Sector during the Pandemic in India:

MSME sector in India was already reeling under huge distress firstly because of demonetisation in 2016, then because of poorly implemented GST in 2017, followed by the prolonged economic slowdown was badly hit by the Pandemic. According to a survey commissioned by All India Manufacturers Organisation (AIM0), India is currently home to over 75 million MSMEs of which close to 25 per cent will face closure, if the lockdown imposed due to the COVID-19 goes beyond four weeks while a whopping 43 per cent will shut shop if it extends beyond eight weeks. The survey conducted among 5000 MSME found that 71% of MSMEs could not pay salary in march. The sector which provides employment to over 114 million people and contributes to more than 30 per cent of the GDP was forced to layoff its migrant workers who defied restrictions of lockdown to travel to their respective homes in another state.

The Government and the Reserve Bank of India came up with stimulus package for the sector and slew of other reforms to tide over the situation. Some of the notable measures announced included Rs 3 lakh crore ($40 Billion) collateral-free automatic loans, Rs 20,000 crore ($2.7 Billion) subordinate debt, and revised definitions of MSMEs to give greater benefits to a larger section of small firms.

Post Pandemic Prediction:

Short Term: In the short term as the Pandemic restrictions remain in place and migrant workers remain away in their home states, it would be very challenging for MSME sector to bounce back. The sector would continue to struggle in coming weeks.

Medium and Long Term: As the virus gets contained and economic revival starts, MSME sector would limp back to normal. Many of them may remain close for ever.

Conclusion:

- The two part blog identified 6 sectors to be particularly vulnerable to a crisis.

- Firms reacted to the crisis by laying off workers, filing for bankruptcy, restructuring, consolidating through mergers and acquisitions and finally changing their business model.

- The time to recovery in these crisis prone sectors vary depends on the stimulus from the Government, liquidity access from the Central Bank and the demand revival in the economy.

- Although the pandemic is a health crisis rather than a financial crisis, the effects are the same.

- The short term impact could be devastating for the firms but in medium and long term as the virus spread is contained things would start to pick up.