Dear Readers,

In today’s blog I want to highlight the looming debt crisis in emerging and underdeveloped nations aggravated due to the global Pandemic which has affected the post war World like no other crisis.

Source: FT

As the Pandemic spreads globally to less developed and emerging nations, economic paralysis and unemployment follow its footsteps. It’s no surprise that the economic fallout of the pandemic in most emerging and developing economies is likely to be far worse than anything we have seen in China, Europe, or the United States. This is not the right time to expect these countries to meet their debt payments, either to private or official creditors such as the IMF, World Bank etc.

With inadequate health-care facilities, limited capacity to deliver big fiscal or monetary stimulus, and underdeveloped or absent social-safety nets, the emerging and developing world is not only on the brink of a humanitarian crisis, but also of the most serious financial crisis in years. Capital has been pulled out of most of these economies over the past several weeks, and a wave of new sovereign defaults appears inevitable in the foreseeable future.

1. Sovereign Debt Crisis:

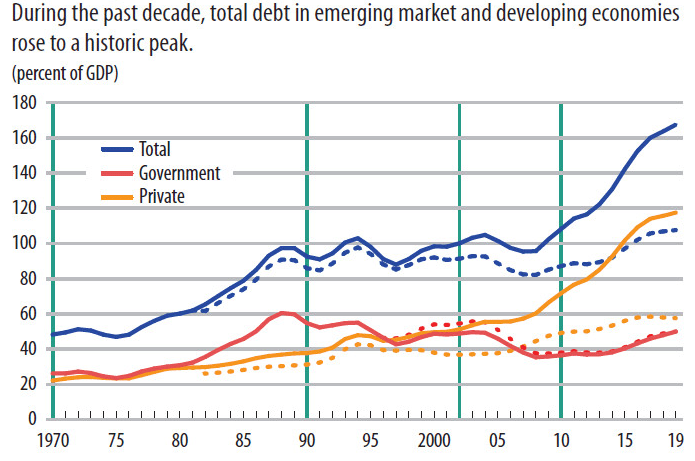

According to Brookings, Emerging and Developing countries together have about $11 trillion in external debt, of which about $3.9 trillion in debt service is due in 2020 including about $3.5 trillion for principal repayments. Around $1 trillion of debt service is due on medium- and long-term (MLT) debt, while the remainder is for short-term debt, normally part of trade finance. It also mentions that the 74 poorest countries estimated by World Bank’s International Development Association (IDA) have around $36 billion due for payments in coming months as part of medium- and long-term (MLT) debt. It would also be fair to mention here that some of the countries such as Argentina, Venezuela, Lebanon, Eastern European and African nations were experiencing a slow down in economy and debt payment issues prior to the Pandemic.

a. Low interest rate spurs lending:

The low interest era of the past decade in the developed world, primarily drove Emerging countries, state owned corporations and private firms in those countries to borrow cheaply from international investors, who were searching for higher returns and were ready to gobble up the debt.

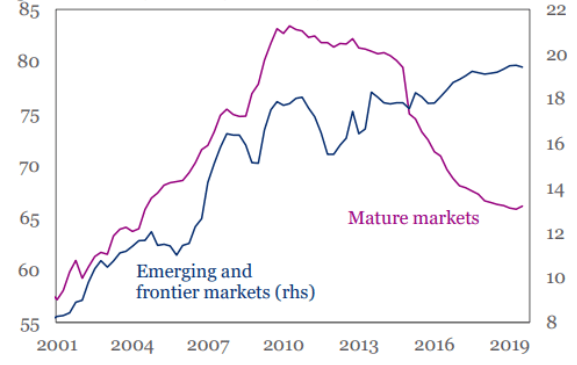

Source: IMF

The Pandemic has hit this investor- investee alliance hard. Economic activity came to a grinding halt severely affecting the revenue stream of the Government of these countries along with the corporations. The debts of recent years are mostly packaged as bonds and placed with clients in pension funds, family offices, hedge funds etc. These entities have their own interests and payments to be done which make the restructuring of debt very difficult. Argentina’s multiyear legal dispute with hedge fund Elliot Management is known to all and how at one point of time, Argentina’s naval vessel was seized.

b. Currency depreciation aggravates debt crisis:

Another issue with the bonds is the currency of these countries. These countries normally try to issue bonds in a well accepted currency such as the U.S dollar or the Euro to attract the investors. In scenarios like this when investors look for safe heaven and turn towards U.S dollars, the currencies of these nations depreciate a lot and thus it becomes hard to buy dollars to service the debt. The Lebanon crisis recently shows clearly the problem when debt issued in dollars are difficult to repay owing to difficult macroeconomic slowdown and huge currency depreciation.

Source: Yale

2. State Owned Corporation Debt Crisis:

Emerging-market economies are facing a new dilemma as they begin the journey to recovery: How to rescue indebted and crippled state-owned corporations?

Cash-strapped governments in emerging countries such as Indonesia, India, South Africa and elsewhere are forced to bailout corporations such as national airlines, energy utilities and other state businesses paralyzed by virus-related mobility restrictions, collapsing demand and plunging oil prices. The debt risk is putting credit rating companies on alert and prompting nervous investors to sell off assets before the situation gets any worse.

In emerging markets, state-owned corporations are key job creators. They are responsible for 55% of infrastructure investment in those countries, according to the International Monetary Fund, and account for about 60% of non-financial corporate debt, the Institute of International Finance estimates.

State-owned entities make up bulk of corporate debt for many Emerging market countries but these entities are often riddled with:

a. Political Interference & Mismanagement:

Governments create these enterprises to meet their specific goals and mandates, such as serving the people through the delivery of basic utility services such as the delivery of water, electricity, gas, transportation routes that the private sector would not find profitable. However, these corporations are often not adequately funded and have high political interference. These corporations often do things to please their political bosses rather than things which make wise business sense. State-owned enterprises are falling short of expectations in many developing countries, where millions of people do not have access to safe water and reliable electricity.

b. Underperformance & High debt:

Governments also fail to effectively monitor state-owned enterprises. Poor transparency in public banks’ and enterprises’ activities remains an obstacle to accountability and oversight. Public sector banks in Brazil, India and other emerging countries are often used by their Governments as a medium to run pro poor programs. These banks have high level of bad debts as their loan delivery mechanism is flawed. This can lead to a buildup of large and hidden debts with governments having to bail them out, sometimes costing taxpayers billions of dollars.

In these cases, the enterprises tend to underperform relative to their private sector peers. According to IMF data drawn from a sample of about 1 million firms in 109 countries, state-owned enterprises are less productive than private firms by one-third, on average. This weak performance is partially due to poor governance: productivity of these enterprises in countries with perceived lower corruption is more than three times higher than those in countries where corruption is seen as severe.

3. Emerging Markets household debt crisis:

Emerging economies have over the past few decades made access to credit easier for their citizens. This has fueled economic growth and development. China and South East Asian countries have seen unprecedented economic growth in line with the growth of its credit for the household sector. In China the household debt as a percentage of GDP has risen from a modest 17.9% in 2008 to 55.2% in 2020. A whole new market of borrowers and lenders have come up in China which was not present a decade ago. As with China, South Korea has seen a boom in credit over the last few decades, its household debt to GDP ratio is approaching 100% (95.2% in 2020) up from 50% in 2000 and 74% in 2008. In South East Asia, Thailand has seen its household debt to GDP ratio rising from 52.4% in 2008 to 69.2% in 2020. Similarly Malaysia seen a growth in household debt to GDP ratio from 50% in 2008 to 68.2% in 2020. In these emerging economies, increased household debt has in many cases been the result of increased access to global financial capital and robust consumer spending at home, driving significant economic growth in many countries in Southeast Asia.

Source: Household Debt to GDP – IIF & BIS

The 2008 Financial crisis originated in the banking system and required a fix to capitalize the balance sheet of those banks. The crisis today is of a different kind and unless a vaccine is developed and the health issue is resolved, the economy would not get back to its pre-pandemic levels and the debt crisis could snowball into a major financial crisis.

Short Term Solution:

a. Standstill Debt:

The first short term solution would be to put a freeze on loan payment till such countries get back on their feet. G-20 nations decided to freeze on bilateral loans to 76 underdeveloped countries. They have called on private sector creditors — largely banks, bond funds and other commercial lenders — to do the same. Unfortunately there is no international legal provision to force private investors to standstill debts.

b. Refinance Debt:

The second temporary debt relief measure would be to seek assistance from supranational institutions such as the IMF, ADB etc. There are reports that already 90 countries from around different geographies have approached the IMF to access emergency financing instruments. The IMF is currently allocating $250 billion of its $1 trillion lending capacity to its members.

Long Term Solution:

In order to control the debt crisis the long term solution needs to have the following 4 approaches:

a. Improve Tax Collection:

Low-income countries face major public financing shortfalls to meet even basic public expenditure needs. A report from ODI, a think tank shows that significant tax and aid increases will be needed to ensure that all countries can afford the necessary investments in healthcare, education and social protection in order to end extreme poverty by 2030. Many low-income countries can do more to improve tax collection to reduce the need for borrowing. This can be done by expanding the tax base and plugging the loopholes in tax evasion.

b. Manage borrowing and lending better:

Careful management of the opportunities, costs and risks of different sources of borrowing is crucial for low-income countries. It is important to ensure that the credit worthiness of the borrowers are properly studied and follow ups are done to avoid default in debt payment in future. Lenders to low income countries must have necessary clauses in contracts to legally challenge delay and pausing of debt servicing.

c. Improve transparency and accountability:

There is considerable room for improvement in debt transparency and accountability at the country and state corporation level. The uses of the debt should be monitored properly and any divergence from original intended use should be reported. This would help improve the credibility before the lenders and hopefully help get lower spreads in interest rates.

d. Introduce better ways to manage shocks:

The slowdown of the economy in low income countries followed by investors pulling out money and depreciation of currency are the biggest shocks a country can face as they have to service debts denominated in dollars or Euros. The country should try to minimize this shock by better management of its currency through intervention by their central banks.

Stay Healthy and Stay Safe !