Dear Readers,

In my last two blogs on COVID-19 crisis, I had focused on the pandemic, policy action necessary to flatten it, possible scenarios of recovery and suggested lessons to draw from a similar episode called Spanish Flu in 1918-1920. One week has passed since the last blog and the world has lost another 30,000 people at the altar of the virus. The majority of new cases and deaths still come from US and Europe but emerging countries such as Brazil, India, Russia, Turkey, Peru, Saudi Arabia, Pakistan and Mexico have now taken spots among the top 20 most affected nations. These nations don’t have the same level of health infrastructure and resources as developed countries but still then they are determined to defeat the virus. Most of these nations have adopted social distancing norms at great economic cost to stop the spread of the virus. I have tried to analyze how the crisis has affected these nations economically.

- GDP Contraction: According to estimates of IMF the GDP of Emerging markets and developing economies would contract by 1%. While China and India would have low positive GDP growth of less than 2%, most of the other countries under the bracket would experience contraction with positive growth possible only in 2021.

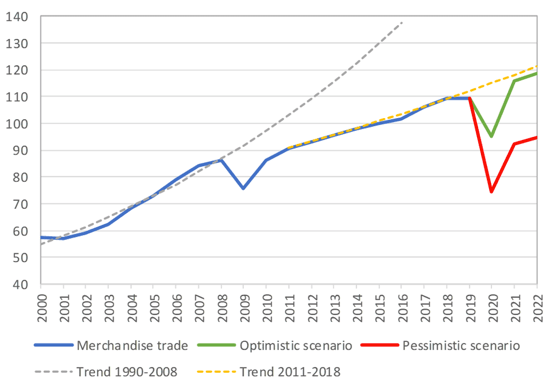

2. Decline in exports and trade: Each Emerging market nation has its own competitive advantages. For instance, India, Brazil, Pakistan, Mexico have a relatively higher proportion of services sector, while Saudi Arabia and Russia rely more on the oil sector. Overall Global Trade was already slowing in 2019 before the virus struck, weighed down by US-China trade tensions and slowing economic growth. According to estimates by World Trade Organization World merchandise trade registered a slight decline for the year of ‑0.1% in volume terms after rising by 2.9% in the previous year. Meanwhile, the dollar value of world merchandise exports in 2019 fell by 3% to US$ 18.89 trillion.In contrast, world commercial services trade increased in 2019, with exports in dollar terms rising by 2% to US$ 6.03 trillion. The pace of expansion was slower than in 2018, when services trade increased by 9%. The below chart shows a region wise trend of Exports and Imports between 2015 and 2019 Q3.

The WTO has estimated two different scenarios for recovery. (1) a relatively optimistic scenario, with a sharp drop in trade followed by a recovery starting in the second half of 2020, and (2) a more pessimistic scenario with a steeper initial decline and a more prolonged and incomplete recovery.

Source: WTO

After the financial crisis of 2008-09, trade never returned to its previous trend, represented by the dotted grey line in the above chart.

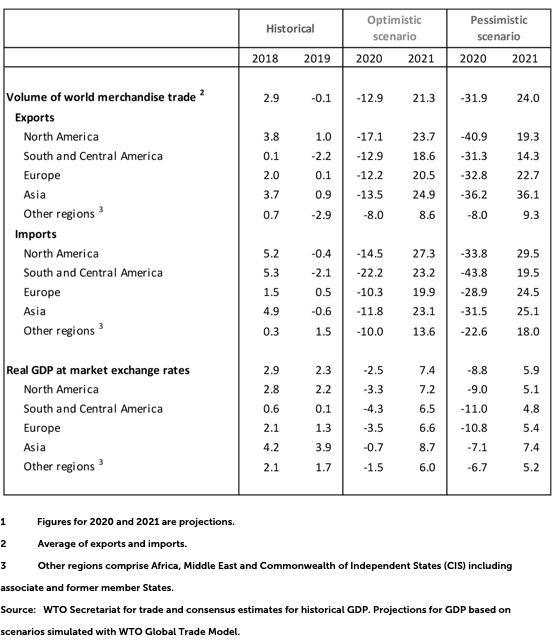

The chart below shows region wise projections of merchandise trade based on the two scenarios.

Under both scenarios, all regions will suffer declines in exports and imports in 2020.

Services are not included in the WTO’s merchandise trade forecast, but with social distancing norms most of them would be impossible. Unlike goods, there are no inventories of services, as a result declines in services trade during the pandemic may be lost forever. Services are also interconnected, with transport enabling an ecosystem of other recreational activities. However, some services may benefit from the crisis. This is true of information technology, e-commerce and online deliveries demand for which has boomed as people work from home and socialize remotely.

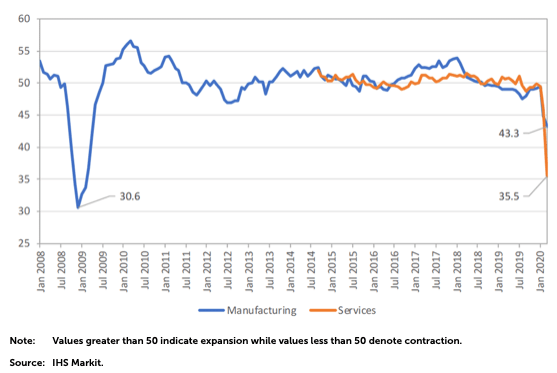

The impact of the COVID-19 outbreak on international trade is not clear yet in most trade data but some timely and leading indicators may provide clues about the extent of the slowdown and how it compares to earlier crises. Indices of new export orders derived from Purchasing Managers’ Indices (PMIs) are particularly useful in this regard. The JP Morgan global PMI for March showed export orders in manufacturing sinking to 43.3 relative to a baseline value of 50, and new services export business dropping to 35.5, suggesting a severe downturn.

3. Unemployment due to COVID-19:

The crisis is causing an unprecedented reduction in economic activity and working time. According to International Labour Organization (ILO) “No matter where in the world or in which sector, the crisis is having a dramatic impact on the world’s workforce”. While the exact number of unemployed due to the Pandemic is difficult to estimate due to unavailability of credible data in all affected countries, a rough estimate based on working hours was done by ILO.

The estimates of hours lost for the first quarter stand at 4.5 per cent (equivalent to approximately 130 million full-time jobs, assuming a 48-hour working week) compared to the pre-crisis level (the fourth quarter of 2019). The estimated decline in work activity in the first quarter of 2020 in different regions is uneven.Whereas the number of hours worked in the first quarter of this year declined by 6.5 per cent in Asia and the Pacific (driven by an 11.6 per cent decline in EasternAsia) compared to the last quarter of 2019, all other major regions saw declines of less than 2 per cent.The decline in working hours in the second quarter is now expected to be even worse than initially estimated. Based on estimates from 22 April 2020, global working hours in the second quarter are expected to be 10.5 per cent lower than in the last pre-crisis quarter. This is equivalent to 305 million full-time jobs.

While the situation has worsened for all major regional groups, lower-middle-income countries are expected to register the highest rate of hours lost, at 12.5 per cent. Among the most vulnerable in the labour market are 1.6 billion informal economy workers who are significantly impacted by lockdown measures and/or working in the hardest-hit sectors. In lower and lower middle income countries informal workers account for more than 85% of the total unemployment.

Source: ILO (International Labour Organization)

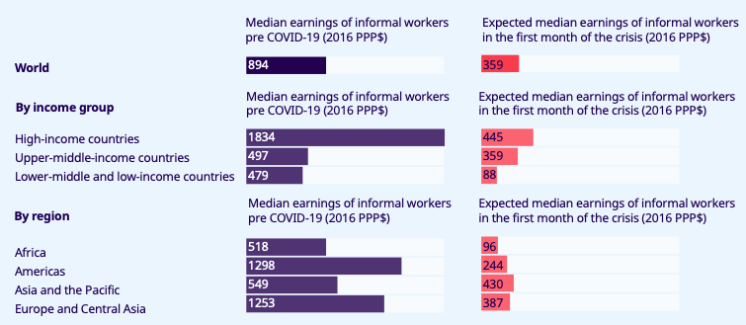

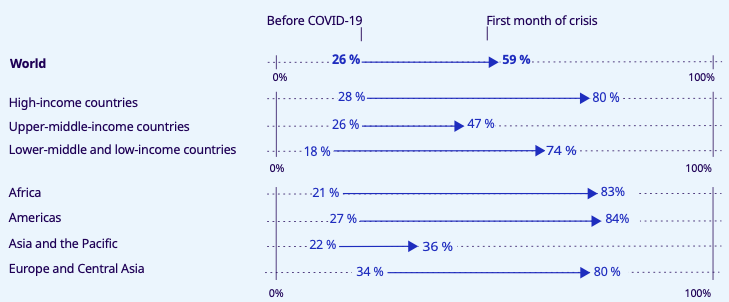

The first month of crisis is estimated to result in a decline in earnings of informal workers of 60 per cent globally and by more than 80% in emerging economies.

Source: ILO (International Labour Organization)

This has the unwanted consequence of pushing millions of workers in informal economy into poverty. An estimate done by ILO during the first month of the crisis shows a huge jump with more than 70% workers in lower-middle and low income countries under the risk of falling back into poverty.

Source: ILO (International Labour Organization)

4. Emerging Markets Inflation Scenario:

Many central banking systems, including the European Central Bank, U.S. Federal Reserve, Reserve Bank of India etc develop their monetary policy around price inflation targets, aiming to keep consumer prices rising at a stable level. However the current unprecedented crisis needed an equally unprecedented monetary policy response. The immediate effect on consumer price indices (CPI) across emerging economies from the COVID-19 crisis is likely to be moderate. In the medium to longer term, however, as aggregate demand recovers, the economy would push up against capacity constraints leading to price rise.

5. Financial Sector Implications:

Until now I had focused on broad Macroeconomic areas and their fallout. I would now focus on the implications of the Pandemic and the policy response on the Macro-finance areas. According to IMF Financial Sector stability report of April 2020, the proportionality of impact on the emerging markets in compare to the developed world has been quite severe.

a. Emerging market sell off:

An unprecedented combination of external shocks (COVID-19 pandemic, oil price decline, increased global risk aversion, and a prospect of global recession) led to a broad-based sell-off in emerging markets. Emerging market equity prices have fallen by about 20 percent, on net, since mid-January despite the most recent rebound after policy actions of central banks in US and Europe rallied those markets.

Source: Bloomberg Finance L.P.; JPMorgan Chase & Co; and IMF staff calculations.

The breadth of outflows—in terms of the number of affected countries—was the largest since the global financial crisis. The depth of outflows was significant for many countries, with South Africa and Thailand witnessing outflows greater than 1 percent of GDP in just two months. Moody’s downgraded South Africa’s local currency rating to sub-investment grade, raising the specter of further outflows by benchmark driven investors. Retail outflows surged more than institutional investors.

Source: Bloomberg Finance L.P.; JPMorgan Chase & Co; and IMF staff calculations.

The reversal of bond portfolio fund flows was broad-based, but relatively worse for hard currency bond funds.

Source: Bloomberg Finance L.P.; JPMorgan Chase & Co; and IMF staff calculations.

To mitigate the impact of outflows on domestic economies, Emerging Market Central Banks have stepped up currency interventions, provided liquidity support to the bond market and to the banking system, and sought to establish swap lines with the US Federal Reserve and the European Central Bank.

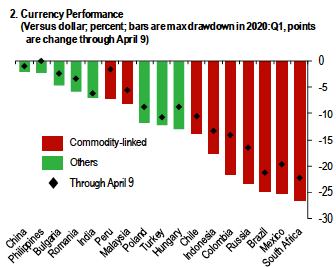

b. Currency devaluation:

Currencies of commodity-producing economies such as Brazil, Mexico and Russia tumbled by more than 20 percent against the US dollar in the first quarter of 2020 Currencies of other emerging markets have been relatively less affected, due to stronger currency interventions by the Central Banks, as well as lower external vulnerabilities.

Source: Bloomberg Finance L.P.; JPMorgan Chase & Co; and IMF staff calculations.

C. Rise in borrowing cost:

Spreads of dollar-denominated emerging market sovereign bonds rose to nearly 700 basis points by the end of March—the highest level since the global financial crisis—although they have narrowed in recent weeks. But for some weaker economies, the current shock was particularly severe as the number of distressed sovereign issuers (those with spreads over 1,000 basis points) rose to record levels. Oil-importing economies have generally fared better, but lower remittances, reduced external funding availability, and lower external demand may outweigh the positive impact of lower oil prices.

Source: Bloomberg Finance L.P.; JPMorgan Chase & Co; and IMF staff calculations.

d. Emerging Markets worse off than 2008:

The sudden stop in economic activity and portfolio outflows, together with the oil price shock, represent a severe stress test for many emerging market economies, especially as many of them entered the COVID-19 crisis with weaker initial conditions than in 2008:

I Rising Debt to GDP ratio – Emerging market bond issuers are much more levered now than they were in 2008, and they include new issuers with a larger dependence on oil and other commodities (Middle east Oil dependant countries)

Source: Bloomberg Finance L.P.; JPMorgan Chase & Co; and IMF staff calculations.

II Tight Fiscal Conditions :Second, many major emerging market economies have less policy space. Real policy rates in most emerging market economies are now lower than before 2008, especially for those with traditionally much higher interest rates (such as Brazil). Fiscal policy space is generally more constrained as well, with debt at significantly higher levels (as in Brazil, China, and South Africa) and wider structural budget deficits (India).

The sharp decline in output and sudden increase in borrowing costs could hurt Emerging economies with limited fiscal space, high financing needs, or external financing vulnerabilities, which include Brazil, India, South Africa, and Turkey. Additionally, economic output decline is also likely to be meaningful for Mexico and Russia. Oil exporters are at risk, given the nearly 60 percent oil price collapse in the first quarter of 2020, with OPEC members, Russia, and Saudi Arabia being most exposed.

Source: Trading Economies

As a result of these pressures Mexico, South Africa, and several Middle Eastern economies were downgraded or put on negative outlook by rating agencies. On the positive side, some economies have large foreign currency reserves and other buffers that can be used to absorb these shocks.

Overall, the sharp tightening of global financial conditions since the COVID-19 outbreak, together with the significant downward revision by the IMF of the 2020 global growth forecast from 3.3 percent in the January 2020 World Economic Outlook Update to –3 percent in the April 2020 WEO, shifted the near-term distribution of global growth dramatically to the left. This shift implies a significant increase in downside risks to growth and financial stability.

One thought on “COVID-19: Macroeconomic and Financial Crisis in Emerging Economies”